A single financial mistake can quietly unravel years of wealth-building even for India’s richest families. It’s a myth that large fortunes are immune to poor decisions. In 2025, with economic uncertainties such as [specific economic factors], tax reforms, and shifting market cycles, even affluent families must stay alert and disciplined. Most often, it isn’t the obvious errors that hurt; it’s the overlooked details and assumptions that go unchecked.

If you belong to a high-income household or are managing inherited wealth, recognising these financial mistakes to avoid can protect your capital, preserve your legacy, and improve decision-making for future generations. This guide dives into the top errors rich families make and how to strategically avoid them.

5 Common Financial Mistakes Rich Families Must Avoid

Wealth can be lost just as quickly as it is built, especially when key details are overlooked. These five mistakes often go unnoticed until they become expensive problems.

1. Financial Mistake of Overspending and No Wealth Budgeting

The belief that “I have enough, so I don’t need a budget” is a dangerous mindset. Many families continue lifestyle upgrades, impulse investments, and big purchases without assessing whether their income supports it. The financial mistake here is assuming that capital will never deplete, but even an ₹80 crore portfolio can’t survive unchecked withdrawal patterns and market dips.

How to correct this mistake:

- Link your spending to your portfolio’s actual income, not potential appreciation

- Use dynamic budgeting tools to review and manage high-cost categories

- Define limits for luxury, travel, and estate maintenance to avoid cash crunches

- Keep emergency funds that aren’t tied up in long-term or illiquid investments

One of the most urgent financial mistakes to avoid is believing that budgeting is only for middle-income households. In fact, the wealthier you are, the more structured your spending needs.

2. No Succession Plan or Family Governance in Place

The second generation loses most family wealth not because of theft or fraud, but because of poor planning. No succession blueprint, unclear roles, or the absence of mentorship often leads to disputes, bad investments, and unmanaged inheritance. This is one of the most common financial mistakes among affluent Indian families.

Smart planning approaches:

- Set up family governance structures, like a family council or charter

- Build legal frameworks, like trusts or holding companies, to transfer assets smoothly

- Educate heirs about taxes, investments, liabilities, and philanthropic obligations

- Include them in financial discussions to build experience and confidence early

Succession planning isn’t just about paperwork; it’s about vision, values, and long-term control. If you’re not actively training your next generation, you may be setting them up for failure.

3. Portfolio Concentration in Real Estate and Private Business

Another common financial mistake is overloading wealth into illiquid assets, such as real estate or privately owned family businesses. While both are valuable, they can’t always be liquidated or restructured quickly during emergencies or downturns. What appears to be stable can often block financial flexibility.

Risk control strategies include:

- Maintain no more than 40-50% of your net worth in illiquid holdings

- Allocate the rest across diversified instruments such as mutual funds, equity ETFs, bonds, and global assets

- Regularly assess the ROI of real estate and business assets against market benchmarks

- Use exit or restructuring strategies during favourable market conditions

Among the financial mistakes to avoid, this one can be particularly damaging when sudden liquidity is needed, for healthcare, opportunities, or economic downturns.

4. Poor Tax Structuring Across Assets and Income

Paying taxes is inevitable. Overpaying them is avoidable. Tax inefficiencies are one of the most silent yet serious financial mistakes the wealthy make. Without long-term tax planning, a substantial portion of your return is lost each year.

Tactical improvements for better tax outcomes:

- Use HUFs, private trusts, and other wealth vehicles to segment taxable income

- Stagger redemptions to stay within favourable long-term capital gains brackets

- Invest in debt funds, NPS, sovereign bonds, and instruments with tax benefits

- Involve wealth and tax professionals to anticipate rule changes and exemptions

Ignoring tax planning is one of the most expensive financial mistakes to avoid, especially with the evolving tax code and inheritance policies in India.

5. Managing Wealth Without Professional Support

Many rich families still manage their finances independently or with legacy advisors who may not have updated knowledge or tools. But as wealth grows, so do the risks, regulatory compliance, estate protection, diversification, global exposure, and legal liabilities, all need specialised attention. Seeking professional support can provide reassurance and confidence in managing these complexities.

3 Steps to Take to Avoid Financial Mistakes

Work with a SEBI-registered wealth management company in Gurugram like BellWether

- Consolidate your scattered assets under a structured wealth plan

- Ensure coordination between investment, legal, and tax advisors for aligned decisions

- Use digital tools and reporting dashboards for real-time visibility and control

This is one of the most preventable financial mistakes. Not seeking the right advice may cost you far more than you expect in penalties, underperformance, or lost opportunities. By being aware of these mistakes and taking proactive steps to avoid them, you can empower yourself to protect and grow your wealth.

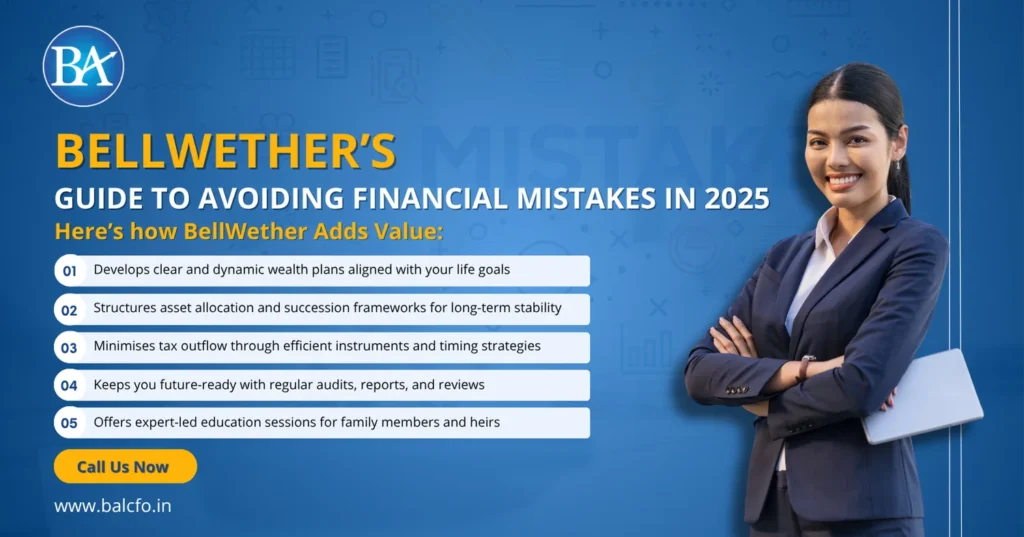

BellWether’s Guide to Avoiding Financial Mistakes in 2025

As India’s trusted wealth management company in Gurugram, BellWether helps affluent families build a long-term financial structure that avoids costly missteps. We understand the complexity of multi-generational wealth and help you simplify it with customised, professional strategies.

Here’s how BellWether adds value:

- Develops clear and dynamic wealth plans aligned with your life goals

- Structures asset allocation and succession frameworks for long-term stability

- Minimises tax outflow through efficient instruments and timing strategies

- Keeps you future-ready with regular audits, reports, and reviews

- Offers expert-led education sessions for family members and heirs

By partnering with BellWether, you get more than just financial management — you get peace of mind, clarity, and a legacy that lasts.

FAQs: Financial Mistake Prevention for Wealthy Families

1. What financial mistake can erode wealth fastest?

Overestimating returns and withdrawing too much from the portfolio is the fastest route to wealth erosion. This mistake, when compounded with poor budgeting, can force families to liquidate core assets and miss out on compounding growth.

2. Why is tax planning a key financial mistake to avoid?

Without structured tax planning, wealthy families lose lakhs in preventable tax outflow. Instruments like trusts, indexation benefits, and asset timing can legally reduce your tax burden and increase post-tax returns.

3. Is a lack of succession planning a financial mistake?

Yes. Not having legal documentation, nominee structures, or clear asset distribution leads to family disputes and delays. A professional wealth manager ensures assets move smoothly to the next generation with tax and legal efficiency.

4. How can professional advisors help avoid financial mistakes?

They offer cross-functional insights across investment, tax, legal, and estate planning. Professionals spot risks, use tested frameworks, and bring global strategies tailored to Indian families, preventing errors that DIY methods often overlook.

5. Are financial mistakes avoidable even in unpredictable markets?

Yes, if you have proactive reviews, asset diversification, tax optimisation, and a long-term plan in place. Predicting markets isn’t possible, but preparing for them is.